The AI-Enabled Services Opportunity

AI-enabled services may be the most attractive application-layer opportunity in AI right now. Here's the 8-point scorecard I use to rank every category, and where the blue oceans still are.

Over the past few months, I’ve been building a thesis on why AI-enabled services may be the most attractive application layer opportunity in AI, why some entrants still won’t produce venture scale outcomes, and which specific markets remain wide open. This post pulls the full argument together in one place.

I’ve seen services from both sides — as a SaaS CEO who used professional services as a strategic differentiator at Gigya, and now as an investor watching AI collapse the old line between software and services. Here’s where I’ve landed.

Why services, why now

The first-order case is clear: AI can transform a historically difficult category.

Traditional services businesses suffer from low margins, inconsistent quality, limited scalability, and weak NPS. Labor is the product, and labor is hard to hire, train, and keep consistent. AI-enabled services can flip that model.

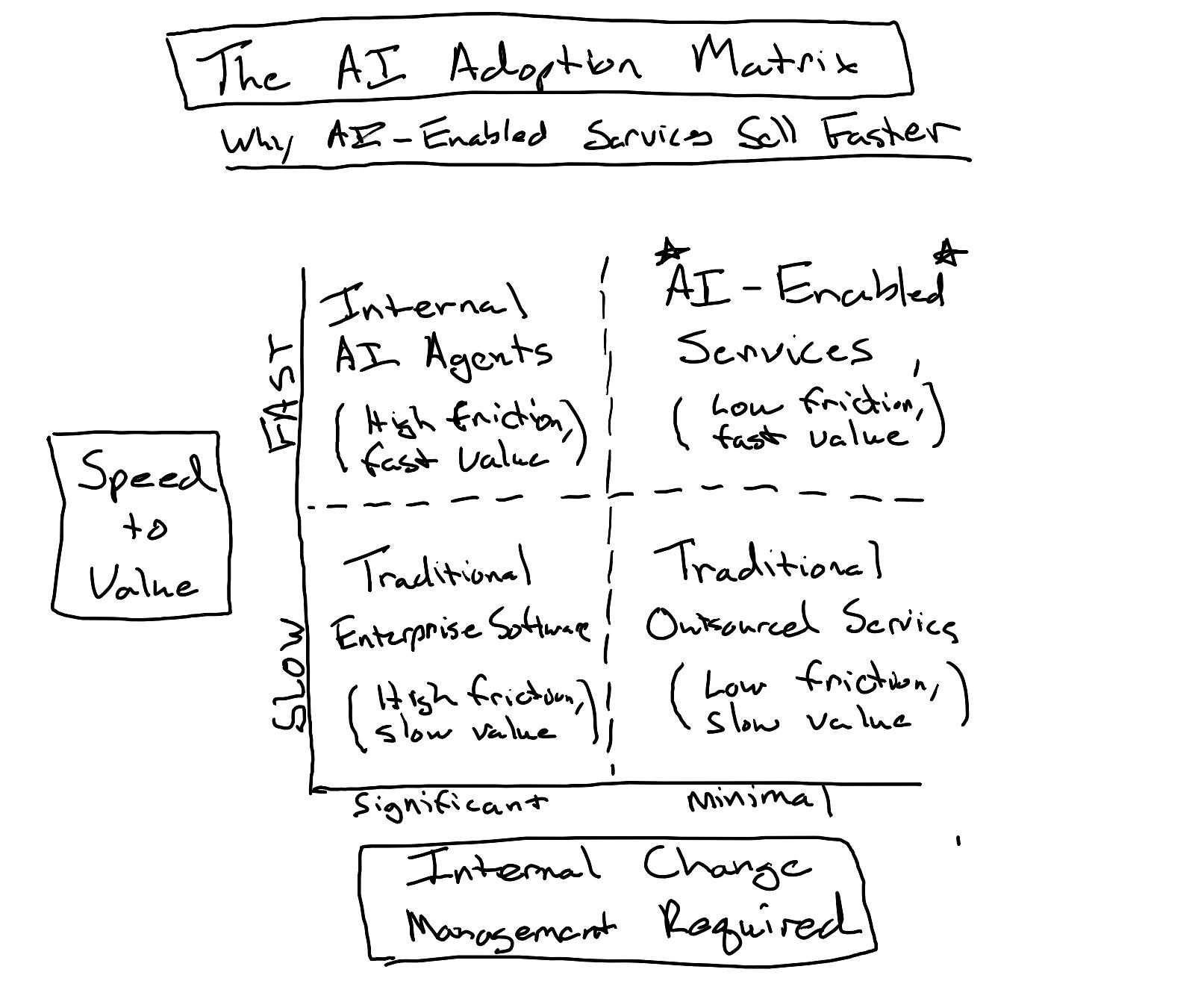

But the bigger unlock may actually be enterprise adoption.

Selling AI agents directly into an organization often requires multi-stakeholder buy-in, change management, and anxiety around job displacement. That friction is slowing growth for many agent startups.

Services markets are different. They are already outsourced.

The enterprise has already decided it doesn’t want to do this work in-house. It already buys the outcome, not the tool. That means faster sales cycles, quicker time to value, and far less internal change management. The AI can operate inside the vendor’s four walls, with FDE style customization handled in the background rather than pushed onto the customer.

For founders, the conclusion is a little counterintuitive: the best way to sell agents into the enterprise may be to not sell agents at all.

The 2x2 below is how I think about it. Internal AI agents deliver value fast but drag change management along with them. Traditional enterprise software is slow on both counts. Traditional outsourced services are easy to buy but slow to improve. AI-enabled services sit in the quadrant enterprises actually want: minimal change management, fast time to value.

Margins are not moats

Now the catch.

Many AI-enabled services startups will have better gross margins. Fewer will have real moats with compounding advantages: better product. Better data. A tractable market. Higher switching costs. Recurring revenue.

Margin improvement is what AI does out of the box. Point a model at a labor-heavy workflow and the cost line drops. But if that’s all that happens, your advantage lasts exactly as long as it takes the next founder (or the incumbent you’re disrupting) to apply the same models to the same workflow.

That’s the test in the 2x2 below. High AI impact with no compounding durability? Cost cutter. Durable business where AI doesn’t materially improve the service? Sticky, but not AI-native. The venture-scale outcomes live in the top right — where AI improves both the service and the durability of the business.

Founders should look for categories where AI improves both the service and the durability of the business.

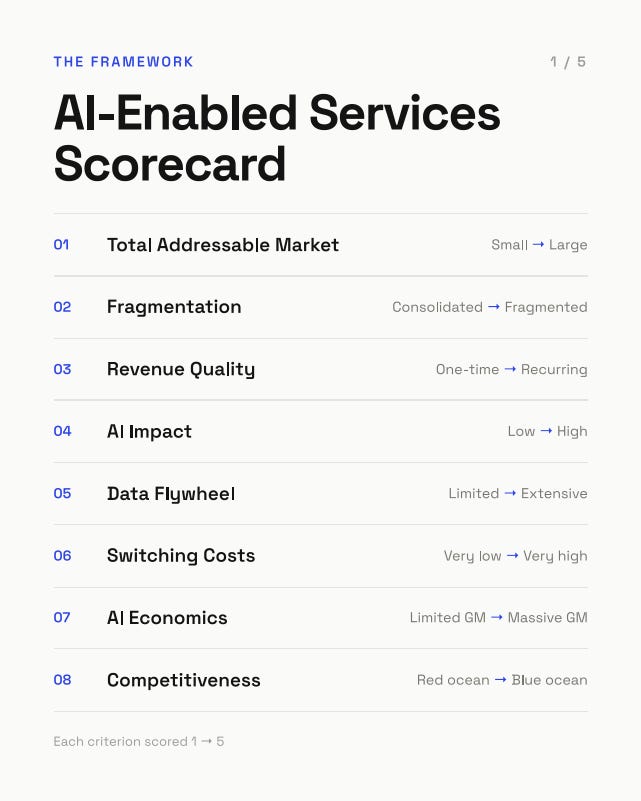

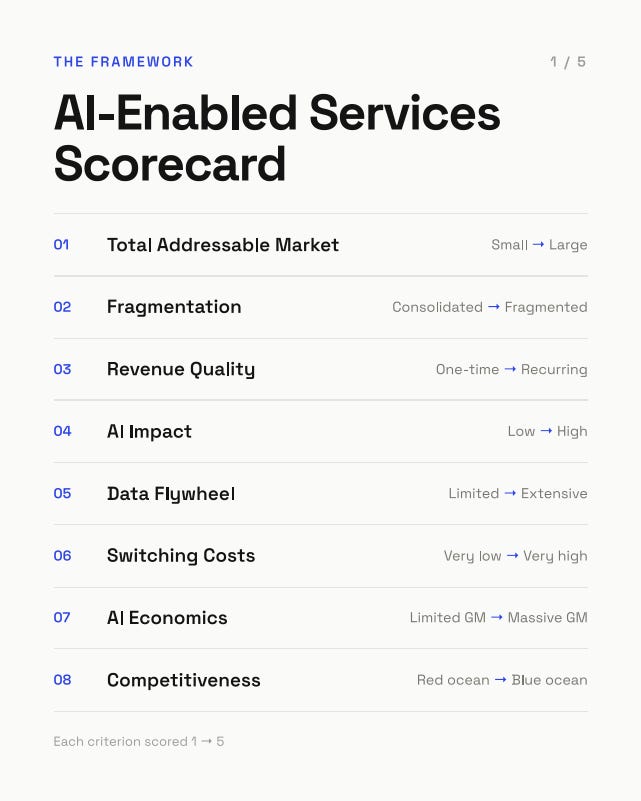

The scorecard

To evaluate AI-enabled services companies — and entire categories — I use an 8-criteria scorecard, each scored 1 to 5:

Total addressable market. Is the current services market large enough to support a venture outcome?

Fragmentation. Is the market fragmented enough for a new entrant to wedge in?

Revenue quality. Is revenue recurring, or mostly one-time and project-based?

AI product impact. Does AI make the service materially better, not just cheaper or faster?

Data flywheel. Does every customer interaction improve the service?

Switching costs. Once utilized, is the service hard to rip out?

AI economics. Does AI structurally change the gross margin profile — a limited bump, or a massive one?

Competitiveness. Is the category already a red ocean of funded entrants, or still open water?

The first seven criteria tell you whether the business can compound. The last tells you whether the opportunity is still worth entering.

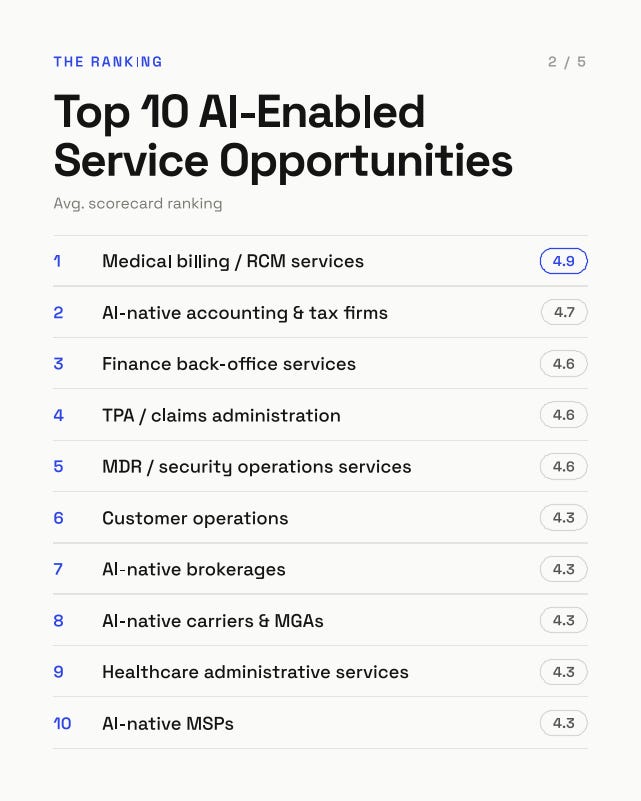

I ran every major services category through it

Using Claude’s Fable model, I ran the full services category list through the scorecard and ranked the results. Two things stood out.

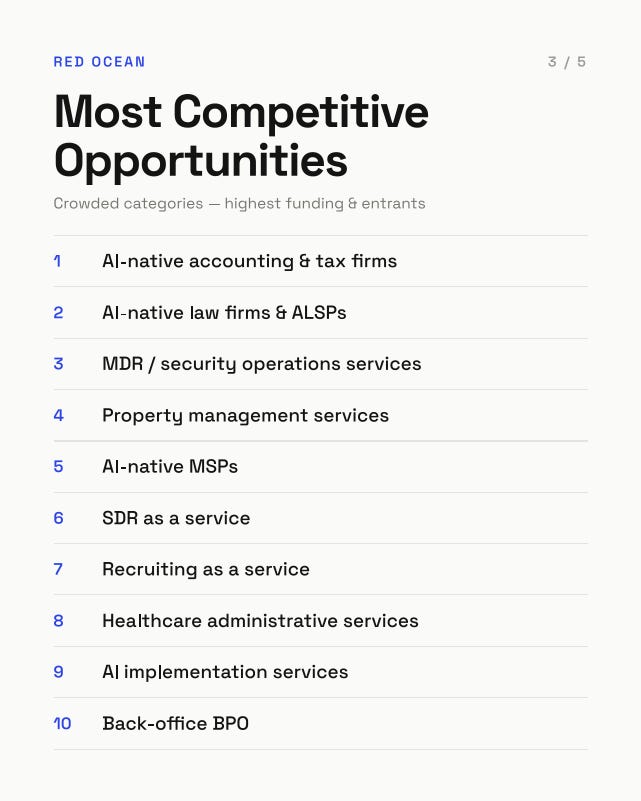

1. The top of the list is a red ocean.

Medical billing / RCM services tops the ranking at 4.9, followed by AI-native accounting & tax firms, finance back-office services, TPA / claims administration, and MDR / security operations.

But notice the overlap: accounting & tax, MDR, and MSPs all rank top 10 on score and top 5 on competition. The rest of the most-crowded list won’t surprise anyone reading fundraise announcements lately: AI-native law firms and ALSPs, SDR-as-a-service, recruiting-as-a-service, AI implementation services, back-office BPO. This is where founder and investor attention is concentrated today — rightfully so — and these crowded categories are likely great Series A/B+ opportunities, where execution and distribution will decide the winners.

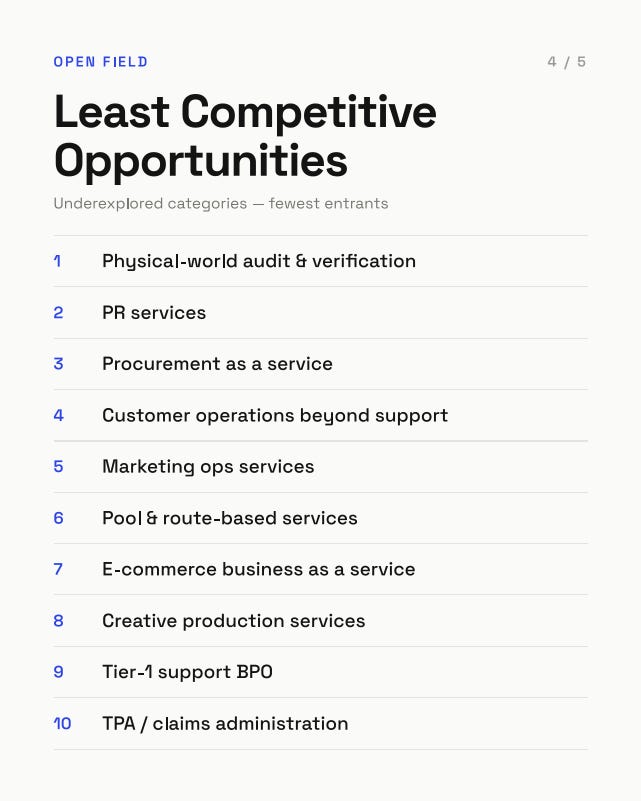

2. Blue oceans still exist.

Good news for seed-stage founders: attractive, less-crowded opportunities are still out there.

Tier-1 support BPO, procurement as a service, and marketing operations all score high with few venture-backed incumbents. And categories that touch the physical world look underserved — customer operations beyond support, physical-world audit & verification, and logistics operators, for instance.

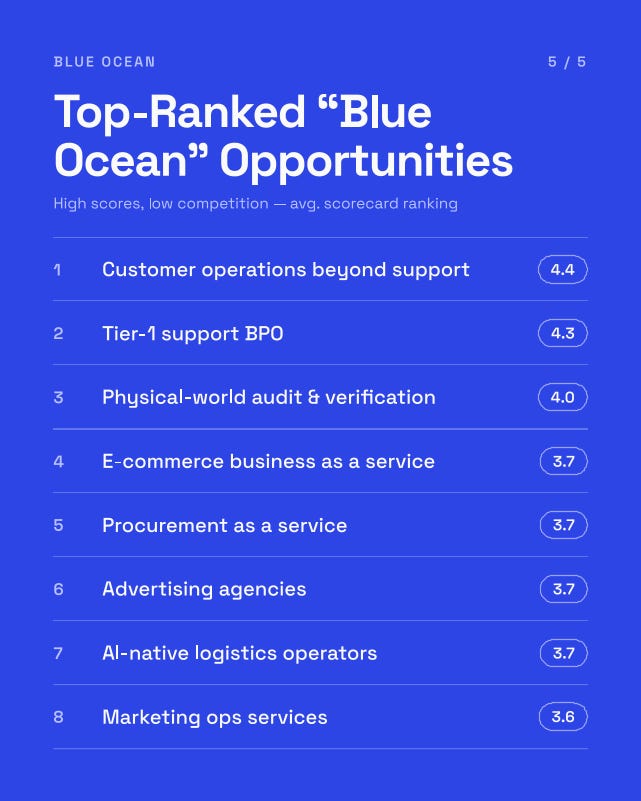

At the top of the blue-ocean ranking: customer operations beyond support (4.4), tier-1 support BPO (4.3), and physical-world audit & verification (4.0).

The bottom line

The most interesting AI-enabled services companies are not just replacing labor with AI. They’re turning service delivery into product, data, workflow depth, and customer lock-in.

Better gross margins are the starting point. Compounding advantages are the company.

One more thing: this scorecard evaluates categories. Whether a specific startup in a category survives contact with Claude, ChatGPT, and Gemini is a different question — that one gets the Defensibility Report Card treatment from my last post. Use them together.

If you’re building in one of these categories, I’d love to learn more. And if you’re operating in one of these markets and think the scorecard got something wrong — run your own category through it and report back.